Under U.S. GAAP, interest paid and received are always treated as operating cash flows. The issuance of debt is a cash inflow, because a company finds investors willing to act as lenders. However, when these debt investors are paid back, then the repayment is a cash outflow.

What is the Statement of Cash Flows Indirect Method?

(The rest is reported as accounts receivable.) Gross profit is reported in the income statement as $500,000. This is also a respectable number, but only $100,000 translates into a positive cash flow, because only some of the inventory purchases were paid in cash. (The rest of the inventory is reported as accounts payable.) The company must still pay some of its operating expenses, leaving only $10,000 cash in the bank. Propensity Company had an increase in the current operating liability for salaries payable, in the amount of $400.

Statement of Cash Flows Direct Method

11 Financial’s website is limited to the dissemination of general information pertaining to its advisory services, together with access to additional investment-related information, publications, and links. For instance, if a company realizes that it will have a cash shortfall in the next month, it can take steps to ensure enough funds are available. To present a clearer picture of the two methods, there are some examples presented below. Get free guides, articles, tools and calculators to help you navigate the financial side of your business with ease.

Maintains an Optimum Cash Balance

- Gain or loss is computed by subtracting the asset’s net book value from the cash proceeds.

- 11 Financial is a registered investment adviser located in Lufkin, Texas.

- Although most standard setting bodies prefer the direct method, companies use the indirect method almost exclusively.

- It’s an asset, not cash—so, with ($5,000) on the cash flow statement, we deduct $5,000 from cash on hand.

- Clearly, the exact starting point for the reconciliation will determine the exact adjustments made to get down to an operating cash flow number.

This is buying back, through cash payment, the equity from its investors. Cash spent on purchasing PP&E is called capital expenditures (CapEx). These investments are a cash outflow, and therefore will have a negative impact when we calculate the net increase in cash from all activities. In the case of Propensity Company, the decreases in cash resulted from notes payable principal repayments and cash dividend payments. The remainder of this section demonstrates preparation of the statement of cash flows of the company whose financial statements are shown in Figure 16.2, Figure 16.3, and Figure 16.4. The investments cost $80,000 (given on the balance sheet) and there was a gain of $10,000 when they were sold (given on the income statement).

Limitations of the Cash Flow Statement

Business events are recorded with income statement and balance sheet accounts like sales, materials, and inventory. It’s laborious for most companies to compile the information with this method. Items that law firm accounting and bookkeeping 101 are added or subtracted include accounts receivables, accounts payables, amortization, depreciation, and prepaid items recorded as revenue or expenses in the income statement because they are non-cash.

In contrast, when interest is given to bondholders, the company decreases its cash. Cash-out transactions in CFF happen when dividends are paid, while cash-in transactions occur when the capital is raised. Together, these different sections can help investors and analysts determine the value of a company as a whole.

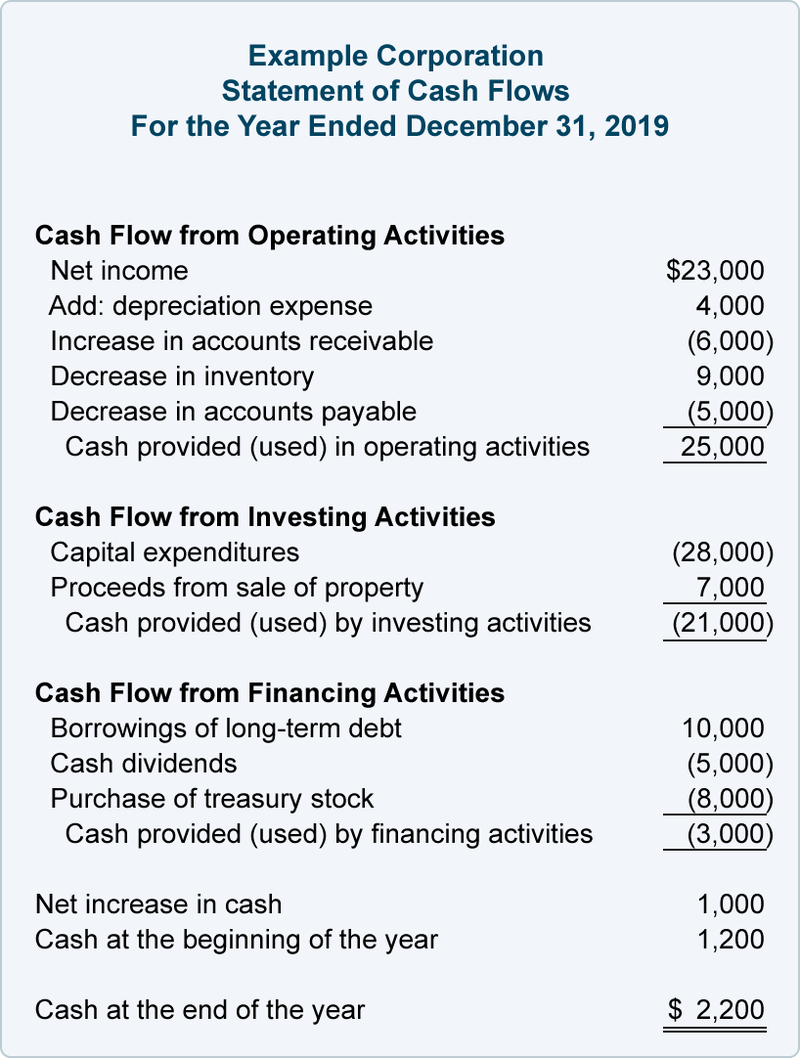

Propensity Company had two examples of an increase in cash flows, one from the issuance of common stock, and one from increased borrowing through notes payable. Each of the three sections is summarized by one number, which is the net cash flows amount. If the summary number is positive, it means that more cash was received than was paid out for that activity during the accounting period. If the summary number is negative, more cash was paid out than was received for that activity during the period.

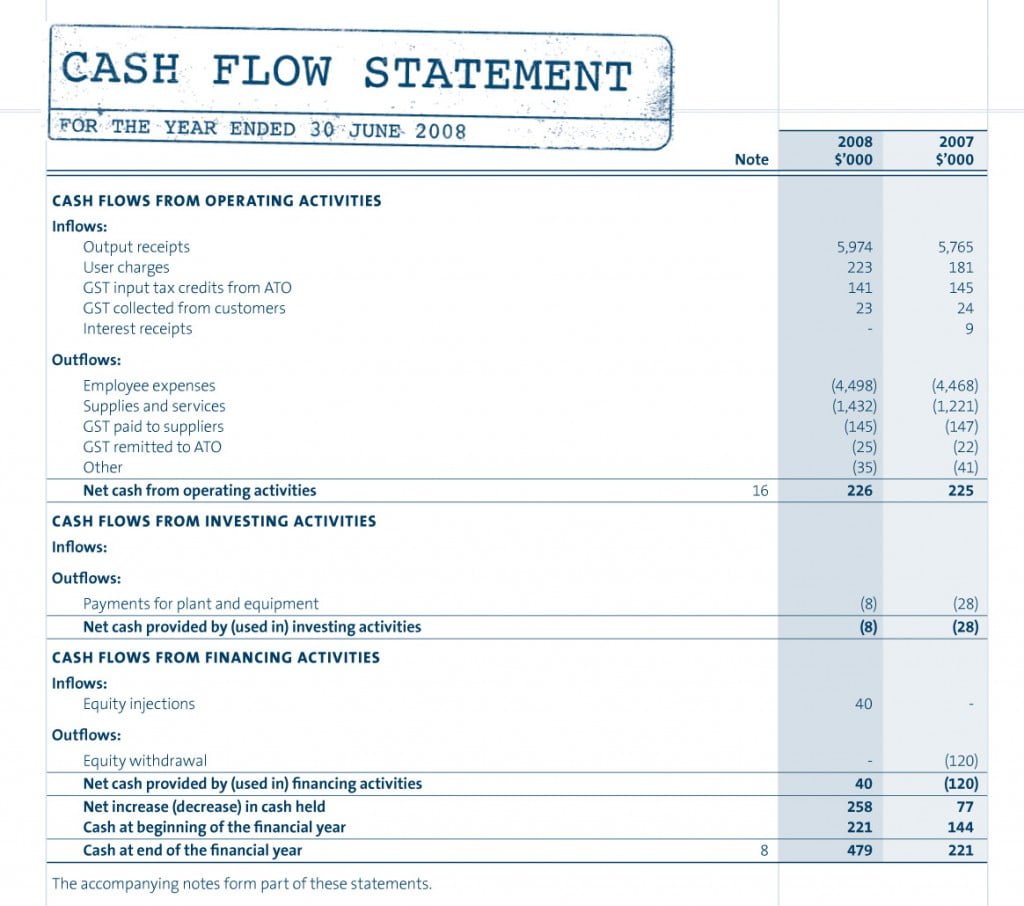

Therefore, businesses prepare a fourth financial statement, the statement of cash flows, to clearly provide information about the sources and uses of cash. The main components of a cash flow statement are cash flows from operating activities, investing activities, and financing activities. As we have discussed, the operating section of the statement of cash flows can be shown using either the direct method or the indirect method. With either method, the investing and financing sections are identical; the only difference is in the operating section. The direct method shows the major classes of gross cash receipts and gross cash payments. The operating activities section is the only difference between the direct and indirect methods.